In this blog, we shall highlight the CBP for the United States.

The North American market retains the largest market share in CBP.

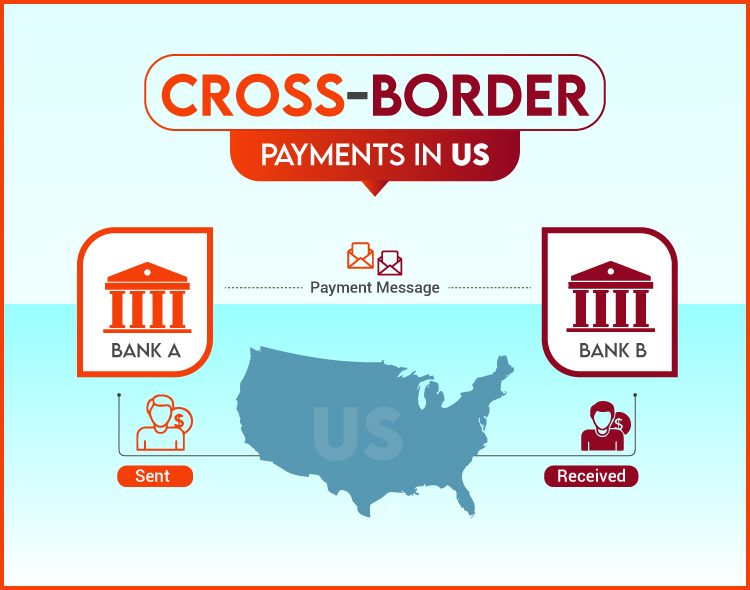

When a person, business, or financial institution sends money to another person, business, or financial institution located in a different country, the transaction is considered a cross-border payment.

Let’s see if we can simplify it for you.

A Beginner’s Guide to Cross-Border Payments

When a consumer pays using a credit card issued by a bank that is not based in the same country as the merchant’s processing account, the issuing bank will charge the merchant a cross-border fee.

Below is a graphical representation as to how Cross-Border Payments work actually.

Let’s pretend you own a deli in New York City and a visitor from Japan comes in for a hot coffee. A cross-border fee will be assessed if the tourist pays for his coffee using a credit card issued by a Japanese bank, as the issuing bank will be located in a nation other than the one in which your merchant account is based.

Latest Read: Can Fintech Survive Without IT Support? Let’s Know With Experts!

A currency conversion fee is different from this one. It’s a separate charge that can be added to the cost of exchanging currencies during an overseas sales transaction or applied independently.

Cross Border Fees: A Historical Overview

In this age of the internet, shopping habits have shifted. We are no longer constrained by the selection available at our neighborhood retailers. These days, all it takes to shop at any of tens of thousands of retailers around the world is a computer with internet access.

There were no international tolls in place before 2005. However, a currency translation fee was added by credit card processing businesses to offset the additional expenses. However, online retailers were avoiding the currency translation tax by employing a variety of workarounds.

Some businesses choose to work with an acquiring bank that allows for transactions in many currencies. Some businesses referred their international clients to local retailers who stocked their products.

A shopper in the United States looking for a wadrobe on a British website might be redirected to a distributor in her own country. A credit card issued by a US bank would then be used to make the purchase, negating the need for a currency exchange.

Read more: Top 10 Fintech CEO Watchlist

Merchants have been required to pay a cross-border fee to MasterCard and Visa since 2005 if they accept foreign credit cards. Regardless of whether or not a currency conversion is required to complete the transaction, the issuing bank still assesses this cost, which is then passed on to the merchant.

How to Calculate Cross-Border Fees

The issuing bank of the credit card used in an international transaction performs two checks:

1. In what country was the credit card issued?

2. In what country is your merchant account located?

The issuing bank will check to determine if you are dealing with customers from outside the country where your merchant account is based. The following is the current pricing structure.

• A foreign customer billed in your currency will incur an additional access of 0.40% (or 40 basis points).

• You will be charged an additional 0.80% (or 80 basis points) when billing a foreign consumer in their local currency.

Let’s revisit the story of a Japanese visitor to New York who relished red sauce pasta. Because he charged an international consumer in US dollars, the concerned person will see a line item labeled cross border fee or foreign transaction fee for 0.40% of the total cost on his monthly credit card processing account.

Exploring the Benefits of US Participation in Standardization

At a CAGR of 5.3% between 2021 and 2027, the global cross-border payments market is expected to expand from its current value of $176.5 billion.

There are many reasons why the United States’ (US) participation in the formulation of standards for international transactions is crucial.

Read : Global Fintech Fest 2023 – Outcomes

- For one, it makes it more likely that the United States will have input into the creation of regulations that will affect its economic sector and its investors. The United States could fall behind other countries that participate in the standard-setting process if it does not.

- Second, the United States’ participation in standard-setting can boost productivity and growth in economies around the world. The United States can ease international trade and lower transaction costs by promoting uniformity in corporate practices across borders.

- Finally, American participation in the standard-setting process may safeguard American consumers and investors. The United States can aid in the fight against fraud and the protection of consumers and investors by ensuring that standards are set in an open and accountable fashion.

Conclusion

The United States, as a whole, is keen on contributing to the process of establishing norms for international trade.

Between 2023 and 2030, consumer-initiated cross-border payments are projected to expand at a rate nearly twice as fast as its business-to-business counterpart. This is in accordance with a market model that focuses on the commercial side of foreign payments and tries to capture their full size.

The United States can advance its economic interests, safeguard its consumers and investors, and promote its values and interests around the world if it takes part in the process of defining international standards.

[To share your insights with us, please write to pghosh@itechseries.com ]