Fintech has experimented with its magic wand in various fields, so how can we corner the money laundering aspect? In this blog we shall be covering how fintech is leveraged to combat money laundering or in other words we can say how fintech is used to fight for AML in a digestable way. With an immense amount of research and impeccable analysis, this slice will give your taste buds the sweetest outcome. Apart from the concept and compliance programs we shall also be discussing the live examples of fintechs in AML along with a few startups which are a helping hand in this domain. Of course, how can a data geek like me forget entailing statistics in this blog?

Come let’s have a look!

Summary

- Introduction

- Anti-Money Laundering in FinTech: What It Means

- Does technology help with Anti-Money Laundering measures?

- FinTech’s AML Compliance Program

- How Serious Is the Money Laundering Peril for FinTech?

- Risk management in FinTech

- What then is the FinTech application of CDD procedures?

- Solutions That Assure Know Your Customer Compliance And Anti-Money Laundering

- Fintech case studies for AML

- 5 Top Fraud Prevention Startups Impacting Financial Services

- Conclusion

Introduction

In order to revolutionize financial transactions, “financial technology,” or FinTech as it is known colloquially, uses software, hardware, and other innovative solutions. About 90% of Americans use FinTech in some capacity to handle their finances, spanning from mobile payment apps and internet banking to cryptocurrency. Using cutting-edge technologies, financial technology (FinTech) enhances and automates financial services. Because technology has advanced and conventional methods are no longer enough, FinTech wants to compete with traditional financial services. FinTech and its solutions are necessary for the financial sector. With mobile banking, mobile payment, cryptocurrency, and bitcoin innovations, fintech has transformed the finance sector. FinTech is subject to rules much like conventional banks are. These laws are anti-money laundering laws.

FinTech must adhere to the AML requirements laid down by regulators, much as other financial industries, because financial crime vulnerabilities exist in all financial sectors. There are also global FinTech regulations that must be adhered to, even if they typically vary from nation to nation. You can read more in-depth information regarding anti-money laundering (AML) for fintech in the rest of our post. FinTech is not new, but the COVID-19 pandemic hastened its development as the demand for contactless payments skyrocketed. Regulators have found it challenging to keep up with this disruptive industry due to the quick adoption and application of new technologies. Regulations are still in their infancy compared to the conventional banking system, making FinTech firms easy targets for financial crime.

Authorities are aware of the dangers that FinTechs face, including those related to human trafficking, money laundering, funding terrorism, and another embezzlement. They are proposing FinTechs to configure security measures to safeguard the American financial system. FinTech enterprises must take strategic steps to mitigate vulnerabilities and proactively alter the regulatory landscape in order to achieve a balance between regulation and innovation. Depending on FinTech’s business model, the kinds of products and services it offers, and the operating jurisdiction, different laws and licensing requirements apply. Similar financial crime laws apply to traditional banks and financial institutions as well as FinTechs that conduct financial transactions, such as shifting money from one organization to another. Similar financial crime laws apply to traditional banks and financial institutions as well as FinTechs that conduct financial transactions, such as shifting money from one organization to another.

Read: How Does Visa Generate Money From International Transactions?

Anti-Money Laundering in FinTech: What It Means

The development of financial crime coincided with technological growth. To lower the danger of financial crime, regulators have some responsibilities at financial institutions. In particular, following the 2008 financial crisis, regulators put in place measures to safeguard financial institutions and clients, such as anti-money laundering rules. If FinTech doesn’t adhere to these regulations, it could be charged with crimes like money laundering, just like traditional financial sectors are. As a result, authorities have the power to impose harsh penalties like fines and disciplinary action. Money laundering damages FinTech companies’ reputations severely, which has undesirable consequences. On the other hand, a vital factor should be taken into account: FinTech companies should select technology-compatible AML solutions because traditional methods are insufficient for them to adhere to AML standards.

Financial crimes have advanced along with technology. Regulators expect financial firms to reduce the risk of financial crime. Following the 2008 financial crisis, regulators implemented protections, including anti-money laundering procedures, to protect financial institutions and clients. If these guidelines are not followed, FinTech companies, like other financial businesses, could be charged with crimes including money laundering. Because of this, authorities have the power to impose severe consequences like fines and disciplinary punishment. Money laundering causes considerable brand damage in FinTech enterprises, which could have a significant impact on businesses. Yet, one crucial point should be kept in mind: conventional methods are insufficient for FinTech enterprises to comply with AML regulations; as a result, FinTech organizations should use AML for FinTech solutions that are compatible with the technology.

Read: A Global Map Of Cryptocurrency Regulations

Does technology help with Anti-Money Laundering measures?

Solutions That Assure Know Your Customer Compliance and Anti-Money Laundering. Artificial intelligence-powered AML solutions make it simple for you to adhere to all rules and regulations while also lowering your financial risk. Financial crime now has more opportunities thanks to FinTech’s development. Those who want to manipulate the financial system are drawn to anonymity and quick money transfers. Like banks, credit unions, insurance providers, and other enterprises in the financial services industry, fintechs are subject to many of the same risks. Thus, FinTechs need to watch out for:

-

Violations of Economic Sanctions

-

Human exploitation

-

Funding of Terrorism

-

Money Laundering

-

Cronyism and Bribery

-

Drug trafficking

FinTech’s AML Compliance Program

No matter how big or little, all FinTech businesses should prohibit users of their goods or services from funding terrorism or money laundering. Financial technology businesses must successfully prevent financial crimes due to the potential use of their services by criminal groups as a means of crime. As a result, AML Compliance Program should not be undervalued by FinTech activities. The AML Compliance Program covers all of the steps taken by businesses at risk of financial crime to prevent it and to comply with regulatory requirements. FinTech must comply with its AML obligations in the territories they serve in order to reduce the danger of money laundering. They are required to establish an AML compliance program in order to comply with FinTech legislation. Otherwise, regulators may reprimand FinTech.

How Serious Is the Money Laundering Peril for FinTech?

FinTech services in the financial sector have brought clients and businesses substantial convenience, and FinTech is constantly expanding and improving. Money laundering issues emerge together with the expansion of fintech. Money laundering is appealing to criminals in FinTech due to the rise in transaction initiation in these systems, limitless money flow, and use of anonymous accounts for transactional purposes. Criminals continue to use this method of money laundering as the use of digital currency increases. Moreover, electronic anti-money laundering has begun to displace traditional anti-money laundering (transaction laundering). This case demonstrates that FinTech companies could be a target for criminal groups engaged in money laundering. All of this data could represent substantial AML threats to the fintech industry. FinTech should follow best practices to avoid criminal investigations, prevent AML/CTF, and mitigate risk.

FinTech offers cutting-edge tools and goods to businesses and customers, like online credit, trading platforms, and AI-driven wealth management. There are several risk algorithms since these services diverge from conventional financial services. Because of this, finTech companies require a unique approach to managing changing risks.

Regulatory Evaluation

Regulations became a significant concern for Fintech as this sector developed and the regulatory environment changed, prompting regulators to communicate their expectations from FinTech. Additionally, if FinTech wishes to operate abroad, it must adhere to several regional legislation.

Online event FinTech has become a possible target for cybercrime as a result of the services it offers, as services like mobile payment may provide dangers like data breaches and network security, which is a significant risk for FinTech.

Taking of Money

With a large volume of payments and quick expansion, FinTech can be exposed to money laundering and theft. As a result, financial technology faces a significant risk of money theft.

Risk evaluation and control in fintech

AML risk assessment can locate the FinTech companies where money laundering is most likely to occur and locate people who intend to fund terrorism. Doing an AML Risk Assessment at FinTech requires achieving goals including identifying risk sources, assessing risk reduction strategies, and managing effective AML / OFAC compliance processes. Key money laundering risk indicators include the form and size of a business, the sorts of clients it serves, the products and services it provides, the channels through which it acquires new clients and interacts with existing ones, and geographic dangers. All of this crucial data should be taken into account when assessing risk in the FinTech industry.

Read: Let’s Dive Deep Into Fintech Vs The Conventional Banking

Risk management in FinTech?

The board of directors at FinTech businesses should be aware of key procedures, internal controls, and risk tolerance. It is crucial to design and record a risk framework that is compliant with regulatory and operational concerns as a consequence of the AML risk assessment. Additionally, as new services are created and new connections with outside parties are made, all risk factors should be taken into account.

Risk-Based Model for FinTech

FinTech faces significant risks, including those related to money laundering, regulatory compliance, and cybercrime, as we have noted. If FinTech does not manage these risks, they may be exposed to unfavorable bad circumstances. They should use the risk-based strategy, one of the most crucial AML/CTF programs while managing these risks. Using the same AML controls for all customers and processes that need to be done to carry out the control processes is insufficient because not all FinTech risk perceptions and each customer’s risk are the same. Instead, a risk-based strategy should be used.

After doing a thorough risk assessment when opening the customer account, the customer should periodically review the customer to determine any new hazards. The two methods that are most frequently used to gauge client risk levels are PEP and adverse media scanning.

Know Your Customer in FinTech

Financial services use Know Your Customer (KYC) procedures as control measures to identify and reduce risks with both new and existing customers. The risk of money laundering, terrorist financing, corruption, fraud, bribery, and other unlawful financial activities is significantly reduced thanks to KYC. Technology advancement also causes changes in crime methods and hazards. For the purpose of identifying and preventing crime threats that organized crime organizations have created through technology, fintech must adhere to KYC rules and anti-money laundering laws.

The Financial Action Task Force (FATF) proposals and European Union Directives both emphasize the value of KYC. In the fintech industry, new clients are screened to get to know them better. Customer information is gathered, and the veracity of that information is then verified. If these checks cannot be conducted or are interrupted, there may be an increase in money laundering concerns.

Customer Due Diligence in FinTech

Information from customer due diligence (CDD) is provided so that businesses can evaluate the risks associated with their clients. Money laundering and terrorism funding are the two biggest customer dangers. Client due diligence is used in the FinTech industry to ensure customers adhere to the rules and laws in force, stop money laundering and the funding of terrorism, reliably supply the services required, and identify and assess odd occurrences and circumstances.

What then is the FinTech application of CDD procedures?

The customer’s information is first gathered. These details include the person’s full name, address, date of birth, place of birth, nationality, marital status, etc. Second, scanning is done to authenticate so that this data can be used if there is a question. Following a review of client activity, Extended Due Diligence is carried out if the customer falls within the high-risk category. Moreover, client screening is done at predetermined intervals. Customer risk may fluctuate as operations continue.

Enhanced Due Diligence in FinTech

Similar to consumer due diligence, enhanced due diligence (EDD) involves gathering customer information. EDD is still unique in that it is exclusively designed for high-risk consumers, not all customers. FinTech can use EDD methods to prevent difficulties from being caused by high-risk consumers or transactions. FinTech should implement a more thorough assessment process for Political Exposed People (PEPs) and their family members or partners. To safeguard your business from financial crimes like money laundering and preserve the reputations of your enterprises, use EDD to identify dangers that the CDD is unable to detect.

Read: Generate AI Images From Text Using DALL-E : A Revolutionary Tool By OpenAI

Adverse Media Screening in FinTech

You can use a service called “adverse media screening” to look for bad press and unfavorable articles about a person or a company. A crucial component of Know Your Customer and Anti-Money Laundering procedures is Adverse Media. Adverse Media is a tool that FinTech uses to identify and guard against business hazards. In order to prevent financial crime and reputational risk, adverse media screening is therefore a crucial component in Fintech organizations. FinTech conforms with EU Directives and FATF recommendations and can quickly screen clients and business partners for adverse media data utilizing adverse media screening software. Adverse media filters might search for high-risk partners and clients.

Daily news publications take place all around the world, making it nearly difficult to manually scan them all. Yet, this news should be carefully scrutinized because you do not want a customer from your FinTech firm to have a poor title. For instance, clients can have committed crimes like human trafficking, tax evasion, corruption, money laundering, or financing terrorism. Because of this, FinTech companies can use Adverse Media to screen their customers and safeguard their companies against threats.

Fintech transaction tracking

Financial institutions’ consumer transactions can be promptly monitored through transaction monitoring. We might even say that the most effective tool for FinTech to combat financial crimes is Transaction Monitoring. They use Transaction Monitoring software to abide by Terrorist Counter-Financing laws. Many financial transactions take place throughout the day at FinTech companies, and these transactions should be scanned. Transaction Monitoring enables this process to be totally automated. With new technology, criminals can carry out money laundering, fraud, identity theft, and terrorist financing on FinTech platforms. For instance, clients can conduct financial transactions on their phones without a lot of security mechanisms thanks to FinTech’s mobile payment services.

This gives crooks a free pass. Transaction Monitoring can stop such crimes by automatically examining transactions. AML Transaction Monitoring software helps FinTech organizations develop various regulations, and each transaction is automatically governed by these rules. The Advanced Protected Area Test Environment allows for the testing of changes made to rules. Using risk-based scorecards, advanced risk assessments can be produced depending on variables like country and currency. There are numerous additional beneficial aspects in transaction monitoring. Due to Transaction Monitoring, FinTech businesses are able to defend themselves from financial dangers, preserve their brand, and stay out of trouble with the law.

Financial Crime Regulations are shifting

The Biden-Harris Administration declared the battle against financial crime to be a top priority for both national security and the economy. Also, the U.S. The ENABLERS Act, a comprehensive anti-money-laundering law, was approved by the House of Representatives in support of President Biden’s anti-corruption campaign. The measure would expand what constitutes a “financial institution,” addressing a gap that has allowed certain businesses to exploit to hide assets and money within the American banking system. The bill would also cover people who work as third-party payment service providers, in addition to art dealers, attorneys, investment gurus, and other financial intermediaries.

If passed into law, FinTechs that provide wire transfers, cash vaults, or payment processing services would be classified as “financial institutions” under the statute. The measure would require some FinTechs and other financial gatekeepers to adhere to anti-money-laundering, customer due diligence, account identification, and client verification procedures in addition to reporting requirements.

Customer Trustworthiness and Risk Control

Growth in the fintech sector depends on speed. For FinTechs, finding a balance between customer ease and regulatory compliance can be extremely difficult. Federal Know Your Customer (KYC) rules are one such instance. These regulations are utilized in the financial sector to assist prevent financial crime.

In order to comply with KYC, businesses must gather enough personal data on new customers during the onboarding process to verify their identities, comprehend the nature of their activities, and determine the likelihood that they will engage in illegal activity. A customer’s request to open an account might be turned down if they represent a high risk.

Problems With Client Identification in FinTech

It is challenging to confirm a customer’s identification during the onboarding process due to the speed at which clients open FinTech accounts. The capacity of a FinTech to acquire new accounts may be negatively impacted by a protracted approval process since potential consumers may switch to a less onerous service. Compliance with KYC criteria is extremely difficult since younger clients tend to have poor credit histories and because fake IDs are becoming more advanced and common.

Cryptocurrencies and other alternative payment methods put FinTech companies at counterparty risk. Crypto payments make it practically impossible to detect terrorist financing, sanctions violations, and other financial crimes because they depend on anonymity and operate in a decentralized system. Yet, FinTechs that manage their clients’ digital wallets are automatically liable for adhering to KYC rules.

Solutions That Assure Know Your Customer Compliance And Anti-Money Laundering

Artificial intelligence-powered AML solutions make it simple for you to adhere to all rules and regulations while also lowering your financial risk.

Read: Global Fintech Interview with Siddhartha Jha, Founder and CEO at Arbol

Here are a few options to help you adhere to all AML and KYC procedures and policies.

1) Transactional Observation – Every transaction your company conducts on a regular basis carries some kind of risk. Due to their responsibility to prevent money laundering, financial institutions must use transaction monitoring software. Without any prior coding experience, business businesses can develop their own set of criteria to automatically identify suspicious and high-risk economic activity.

2) Name screening for money laundering- AML name screening software can assist you in effectively meeting all of the fundamental requirements of sanctions, PEP scanning services, risk-based approach, as well as local and international AML compliance policies. It can also protect your company from any drawbacks or risks that might develop as the transactional course continues to expand. You can also stay clear of legal repercussions by doing this. You can even carry out Customer Due Diligence or CDD and Know Your Customer or KYC transactions with the aid of AML name screening in compliance with the stated duties.

3) Transaction Screening for Anti-Money Laundering- Banks or DNFBPs can quickly examine the information of the sender and receiver with the aid of AML transactional screening software. By tracing the originator and recipient of transactions with the use of this software, businesses may drastically lower the risk of financial crime. Also, businesses can develop their own customized search choices and sophisticated search criteria. The information gathered by this software is organized in a way that produces thorough outcomes without sacrificing accuracy.

4) Negative media screening- Averse media software assists businesses in tracking and monitoring any unfavorable news regarding any of their current or potential customers. One of the crucial elements in the anti-money laundering and customer knowledge processes is adverse media screening. In essence, it aids businesses in recognizing potential hazards and safeguarding against them. News on terrorism financing, the trafficking of weapons, corruption, money laundering, bribery, the smuggling of drugs, human rights violations, and tax evasion are examples of negative media data. While onboarding new customers, financial institutions can comply with AML procedures by running enhanced media screening in addition to PEP scans.

Fintech case studies for AML from our website

5 Top Fraud Prevention Startups Impacting Financial Services

1) New Account Fraud Detection with AimBrain

In order to access the service, newly registered bank account users must go through some basic onboarding, making them a pretty simple target for scammers. Financial institutions use behavioral authentication algorithms, smart alerts, risk assessments, and deep learning technology to prevent significant data breaches. Deep learning is used by the British startup AimBrain, which BioCatch just purchased, to combat new account fraud and account takeover threats. The company’s authentication software combines active voice, imitation, and movement modules with patented passive behavioral ID data to create sophisticated protection for both new and current users.

2) Anti-Fraud Surveillance by Cleafy

The main goal of anti-fraud surveillance is to continuously monitor financial transactions for out-of-the-ordinary or suspicious conduct. Moreover, anti-fraud observation systems make sure that financial institutions quickly identify and eradicate risks while securely preserving the accounts of their customers. Startups everywhere create fraud monitoring systems as a result, which include sophisticated rule-based engines, anomaly detection algorithms, and potent big data analytics. For the financial services sector and other businesses, the Italian startup Cleafy creates a continuous fraud detection and risk assessment program. The adaptable and reliable technology protects data while monitoring operational traffic and cumulative risk scoring. For threat diagnosis, the software also uses real-time deterministic algorithms.

The main goal of anti-fraud surveillance is to continuously monitor financial transactions for out-of-the-ordinary or suspicious conduct. Moreover, anti-fraud observation systems make sure that financial institutions quickly identify and eradicate risks while securely preserving the accounts of their customers. Startups everywhere create fraud monitoring systems as a result, which include sophisticated rule-based engines, anomaly detection algorithms, and potent big data analytics. For the financial services sector and other businesses, the Italian startup Cleafy creates a continuous fraud detection and risk assessment program. The adaptable and reliable technology protects data while monitoring operational traffic and cumulative risk scoring. For threat diagnosis, the software also uses real-time deterministic algorithms.

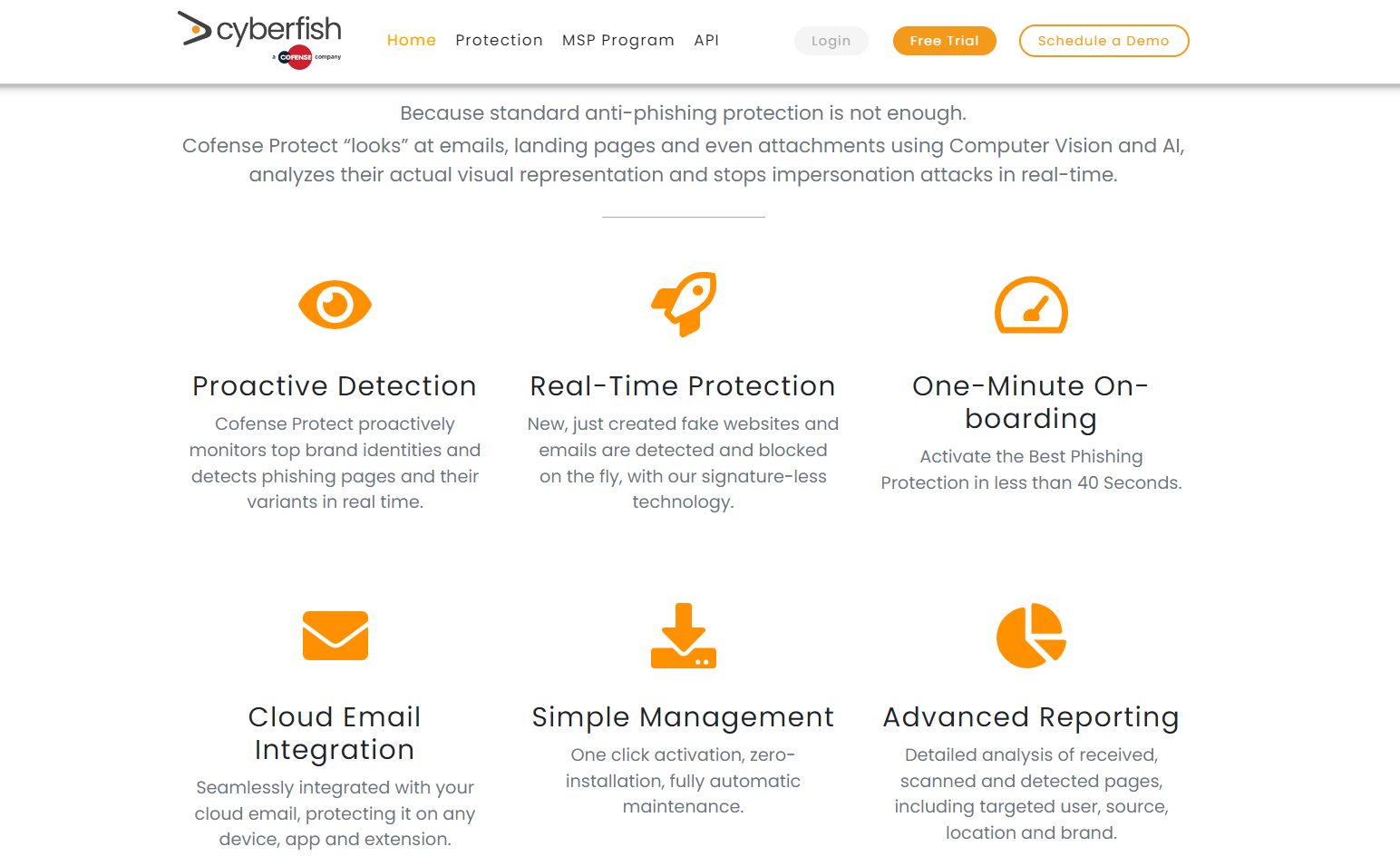

3) Cyberfish: Phishing Defense

Phishing is another method that fraudsters frequently use to get access to banking and financial systems. This technique focuses on acquiring bank credentials using fraudulent phone calls, phishing emails, and the use of social media data. Modern anti-phishing software does in-depth user content analysis, targets and blocks questionable warnings, and offers all-around anti-virus and anti-spam protection. By combining artificial intelligence (AI), computer vision, and contextual training, the Israeli startup Cyberfish creates a platform to eradicate phishing and spearfishing. In order to prevent user impersonation, the platform analyses fraudulent profiles or accounts using proactive detection in addition to cloud email integration.

Phishing is another method that fraudsters frequently use to get access to banking and financial systems. This technique focuses on acquiring bank credentials using fraudulent phone calls, phishing emails, and the use of social media data. Modern anti-phishing software does in-depth user content analysis, targets and blocks questionable warnings, and offers all-around anti-virus and anti-spam protection. By combining artificial intelligence (AI), computer vision, and contextual training, the Israeli startup Cyberfish creates a platform to eradicate phishing and spearfishing. In order to prevent user impersonation, the platform analyses fraudulent profiles or accounts using proactive detection in addition to cloud email integration.

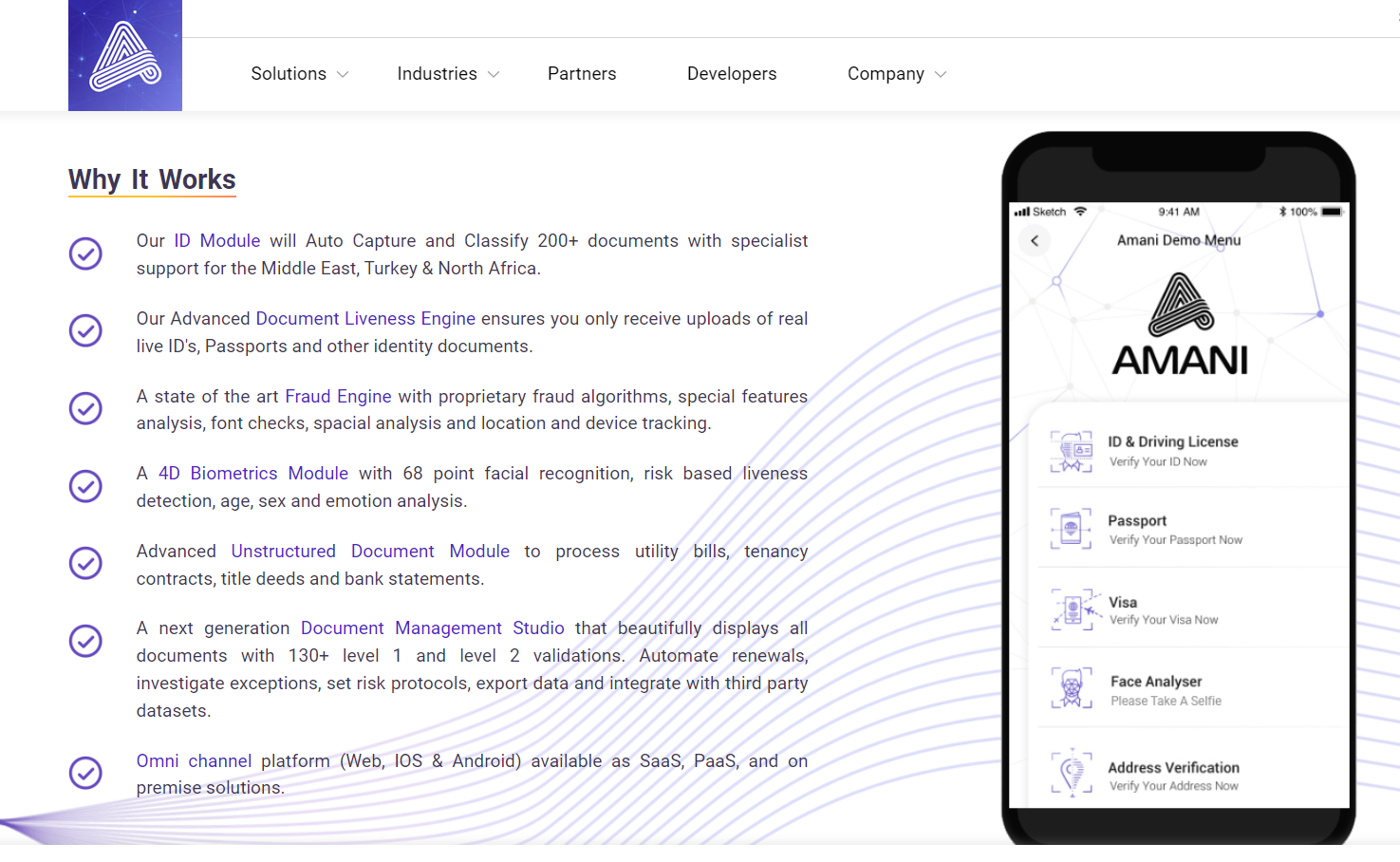

4) Identification Verification with Amani

Individuals and financial organizations conduct many Internet transactions every day. In terms of the security of financial accounts, there are an increasing number of examples of identity theft and fraud occurring globally. Hence, using the power of biometric analysis, artificial intelligence, and machine learning, entrepreneurs aim to improve the identity verification process. For the financial, eCommerce, and other industries, the UAE-based firm Amani creates an AI-enhanced risk management ID verification platform. The platform includes a 4D biometric detection module, an auto-capture ID module, and fraud analysis algorithms. Additionally, it is built on precise standards and safe document management.

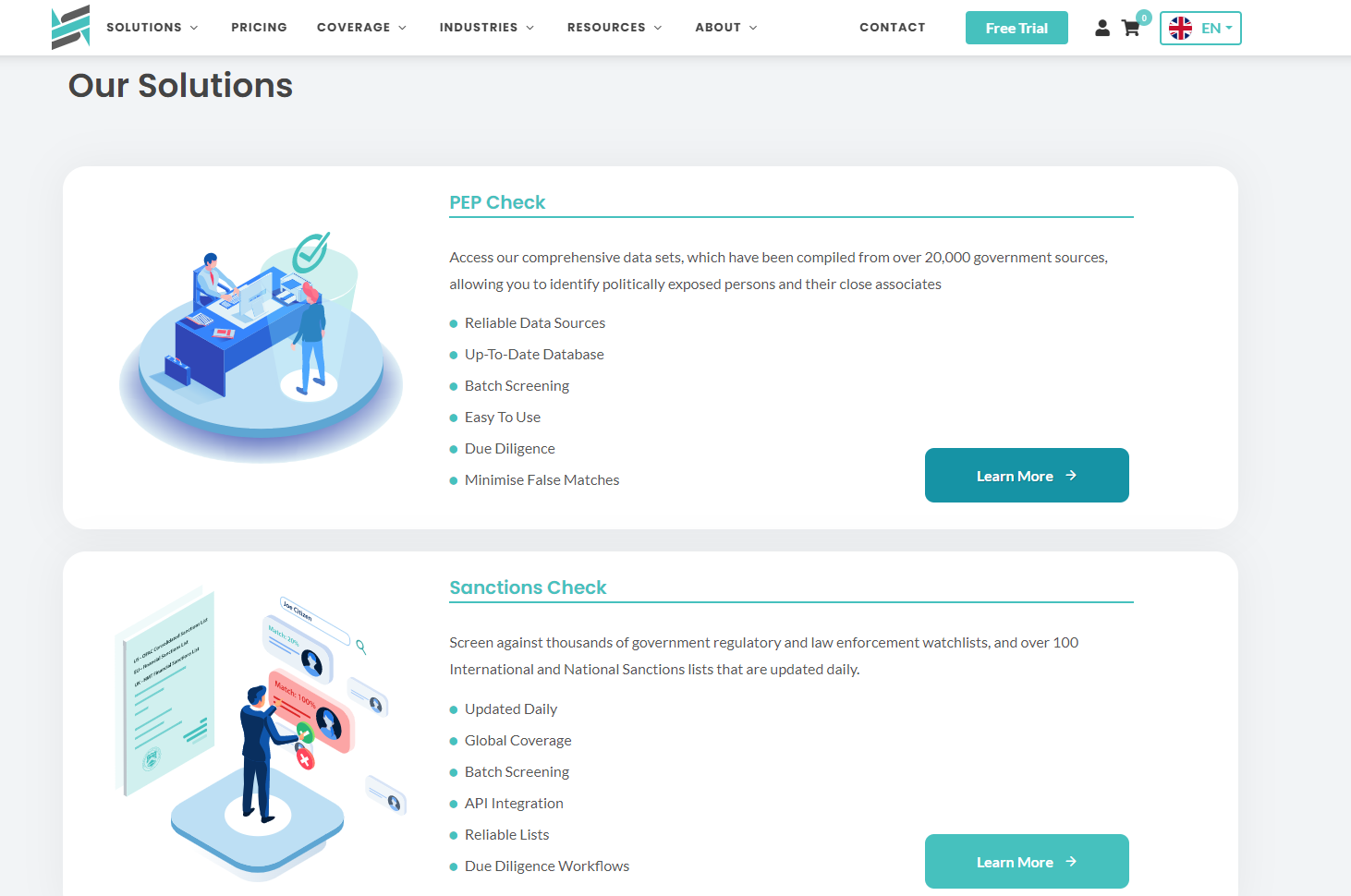

5) Anti-Money Laundering Tool NameScan (AML)

In order to safeguard their clients, banks and financial institutions must adhere to a number of anti-money laundering regulations. These specifications also aid in locating prospective cybercriminal supply chains. Regrettably, traditional AML systems squander precious resources and generate a lot of false alarms. Modern anti-money laundering software uses Blockchain and machine learning to discern between legitimate and illegal behavior with more accuracy and in less time than traditional anti-money laundering software. The Australian start-up NameScan provides financial institutions with anti-money laundering and anti-terrorism financing compliance software. Real-time secure client checks against lists of people with political exposure, sanction, or special interests are made possible by the program. Also, the technology facilitates the scanning of financial records and speeds up the due diligence procedure.

Conclusion

In a nutshell, the AML Compliance Programme encompasses all of the steps taken by businesses at risk of financial crime to prevent it and comply with regulatory requirements. FinTech must comply with its AML obligations in the territories they serve in order to reduce the danger of money laundering.

Fighting financial crime requires AML Compliance Program of FinTech for transparent communication between regulators, FinTechs, and other stakeholders. Creating relationships between various stakeholder groups offers a chance to safeguard the global financial system without endangering the expansion of the industry. FinTechs can assist regulators in better comprehending the quickly changing business, including new goods and services, consumer usage trends, and industry-specific difficulties.

With this intelligence at their disposal, regulators would be better able to create fair, progressive rules that benefit all parties. FinTechs and regulators can communicate about risks, crime trends, and other important patterns of behavior that may help quicker identification of bad actors by expanding on existing collaborations and encouraging new ones. The parties involved must be prepared and eager to identify and put into practice regulatory solutions that strike a balance between innovation and protection and compliance.

Globally there are 217 Anti Money Laundering Software companies, but in this blog, I have discussed the top 5 which I found to be eye-catching and worth scrolling through. I am sure you must have gained some good knowledge while swiping your fingers and rolling down your eyes on your screen.

[To share your insights with us, please write to sghosh@martechseries.com]