What is loan management software?

Loan software automates and administers the loan lifecycle from origination to servicing. It is often referred to as LMS or lending software. The range of loan software comprises account processing, credit scoring, and loan restructuring and disbursement. While an effective loan management system can be a benefit, it must be carefully chosen while taking few factors into account.

What is the most important factor when selecting a loan?

Your Scores and Credit Report

The most important aspect in determining which credit cards you’ll be eligible for and what interest rates lenders are likely to provide you is normally your credit score. Borrowers with strong credit scores typically receive the lowest interest rates from credit card companies.

What are microloans used for?

Individuals who have difficulty getting conventional bank loans frequently choose microloans or microfinancing alternatives. Microloans were selected for a range of business-related purposes, including:

- Launch of a new company enterprise

- Preserving daily cash flow

- Addressing the need for working capital

- Consolidation of debt

- Taking care of daily expenditures

- Paying employees’ salaries, etc.

Latest Read: A Closer Look At Integrated Document Management And Accounts Payable Software

9 Best Loan Software Providers in 2023

- SimpleNexus Mortgage Platform by nCino

- Sageworks Lending

- Salesforce Finance Services Cloud

- Floify

- Sofi

- Bryt

- TurnKey Lender

- LoanSifter

5 key points to select the apt lending software solution for you

Before selecting a lending software solution for your lending firm, keep in mind these five vital factors:

1. Does it offer cloud-based capabilities?

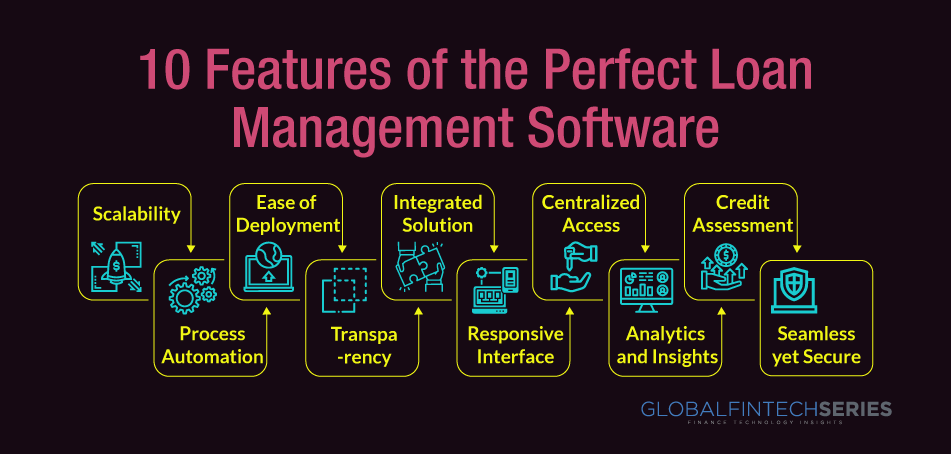

Many businesses are unsure whether to choose a cloud-based software solution or an on-premises one when it comes to software (downloading the software on your computer). In contrast to on-premises solutions, cloud-based lending software solutions have been demonstrated to perform better. Because SaaS firms are committed to creating automation solutions for their customers, offering strong support, and facilitating process easiness, cloud-based solutions are superior. Cloud-based third-party solutions are preferred by lenders all over the world because they provide the cutting-edge technology and regular upgrades needed to stay ahead in the lending industry. Such loan software solutions also provide cost-effectiveness, the most recent security updates, and features that allow access from anywhere.

2. Does it contain features from end to end?

Many of the software choices on the market today only provide a lender with a partial answer to their problems. For instance, the software might have been developed and made specifically to carry out a certain task. This may force you to use multiple tools to handle the various components of loan processing. Because there won’t be any integrated functionality across these products, this may introduce more problems and bottlenecks than it resolves. It is crucial to choose loan software solutions that provide end-to-end services because of this. Such software will assist with everything, including origination, underwriting, maintenance, and reporting.

3. Is the lending software scalable?

The most effective lending software is scalable, versatile, and customizable. So, the same software should be able to meet your needs for automating the lending process whether you run a one-person lending business or a multinational corporation. The price of the software will also increase or decrease depending on how much it is utilized. The majority of software solutions are designed for big businesses that can afford to hire specialists who can manage the software on a full-time basis. They have the means and funds necessary to upgrade in the event that it is necessary. This might not be the case for start-ups, small- to medium-sized lenders, or lenders who are just getting started. So, it is best to choose a software solution with a scale-based cost structure, sufficient scalability, and no significant learning curve.

4. Is the lending software user-friendly?

Software ought to be simple to use. This is true for both the lender and the borrower when using lending software solutions. A potential borrower would probably leave your website or mobile app if they think the software is too difficult in the competitive industry of today. Your lending company presents the software to its customers. It must therefore appear and feel the part. Software may be excessively complicated if it takes a lending specialist more than an hour to understand how it operates during testing. You should not accept anything less than the modern, greatly simplified software UX and UI.

5. Is it capable of accurate credit scoring?

Lenders typically obtain credit scores from independent sources like India’s CIBIL. But what if lending software had the intelligence and capability to automatically obtain credit reports from CIBIL? These days, lending technologies can offer credit scores that get more precise and quick the more they are used. Such software analyses vast swaths of historical data and learns from it using machine learning (ML) and artificial intelligence (AI) technology.

Latest Read: 10 Of The Best Stock Market Podcasts

To sign off

An MFI or NBFC can increase its top line by establishing confidence with its depositors by having a sensible and realistic policy about loans and advances. One easy way to satisfy these requirements is to use debt management software.